Will AI change the world or become another dot-com bubble

In recent years, advancements in data science, predictive analytics, machine learning, and generative AI such as ChatGPT or Dall-E have reshaped the way experts and the general public view Artificial Intelligence (AI). In public consciousness, AI transformed from a science fiction fantasy to an everyday issue. However, we’re not yet at a point where AI can fully replace human professionals.

There is evident enthusiasm for AI, with stock markets reacting in ways reminiscent of the dot-com bubble, though to a somewhat lower extent. While AI has already transformed many industries, it's crucial to recognise that we're still at the beginning of this journey, and we might have only achieved some initial capacities of AI, even though it seems like we're much further along.

The current market enthusiasm for AI comes mainly from the popularity of Generative AI capable of creating texts, images, and programm code. This enthusiasm reflects the potential of AI but also carries risks. Generative AI could be a groundbreaking technology or fail to meet expectations, leading to market instability. It is important to remember that AI is a powerful tool, not a magic solution, and to treat it accordingly.

From science to memes: why the markets got excited about AI

Over the last century, data science has significantly evolved, driven by advancements in computational capabilities and the increasing interest from various industries in utilising new, more powerful and precise tools. Among these tools, AI has emerged as one of the most promising.

AI is not exactly a new technology. It is already widely used and will continue to be used in the foreseeable future. It offers significant benefits across multiple industries and spheres, including governmental policies, economic development, medicine, and disaster prevention. However, the lack of a clear consensus on the definition and scope of artificial intelligence restrains its practical implementation. The transformative power of AI lies not just in the technology itself but in its application (Alhosani and Alhashmi, 2024).

In 2024, we are, however, at a critical stage of technological disruption, with AI being the focus of attention from media and business. The technology is moving from experimentation to the business transformation phase. As seen with the internet and personal computers, broad adoption is necessary for the true transformation. This adoption is happening, as AI is already being integrated into workplaces at an unprecedented scale, with 75% of knowledge workers using AI in their jobs today (Microsoft, 2024).

AI in general excels at handling repetitive and predictable tasks such as data entry, managing bookings, and diagnosing common medical conditions. These tasks, while important, are mechanical. AI steps in not as a replacement for human effort but as a time-saver and a personal organiser.

Analytical AI uses various algorithms to interpret data and make predictions. This predictive analytics approach leverages machine learning and statistical techniques to analyse historical and current data, forecasting future events. For example, traditionally, insurance companies relied on static risk assessment models based on factors like credit scores, income levels, and employment history. While useful, these models often fail to account for the dynamic nature of financial markets and the complex interplay of factors influencing credit risk. Predictive analytics addresses these limitations by incorporating a broader range of variables, including behavioural and transactional data, offering a more comprehensive view (Bonini and Caivano, 2021).

Companies now can access vast amounts of data, including non-traditional sources like social media and transactional data, providing deeper insights. Machine learning algorithms and AI have enabled the development of predictive models that can analyse this data in real-time, offering a more nuanced and forward-looking assessment of, for example, credit risk. These technologies also facilitate the automation of credit decision-making processes, improving efficiency and accuracy (Yuan and Zhang, 2021).

It is crucial to recognise that the excitement in the markets and among the public outside of data science circles is not primarily about analytical AI. The hype is largely driven by generative AI, which can create new content such as text, images, memes, music, audio, and videos from user prompts. Since 2022, generative AI has been one of the most talked-about technologies. However, despite its potential, this technology comes with fundamental limitations and risks often overlooked in mainstream discussions (Goncalo, 2024).

One of the key characteristics of generative AI is its non-determinism, meaning it can produce different outputs even when given the same input multiple times, leading to unpredictability in its results. In industries where reliability is the most crucial, such as healthcare and banking, this unpredictability can be a significant drawback (Goncalo, 2024).

Large generative AI models are trained on vast datasets, often sourced from the internet. This training can inadvertently cause these models to 'hallucinate,' presenting convincingly false information as truth. While generative AI can replicate complex patterns, it lacks the intuitive understanding of the world that humans possess (Goncalo, 2024).

AI in Insurance: A Seismic Shift of Unknown Scale

Predictive analytics is all about what can be correctly and ethically predicted by data. In this aspect, the use of AI raises concerns surrounding privacy, bias, and accountability. In practice, to gain valuable insights, it is necessary to understand the logic of the AI model that makes a prediction. If the user can’t double-check the AI logic, techniques and algorithms, the only other remaining option is to blindly trust AI. This approach doesn’t work when human lives, health and financial stability are at stake.

Nevertheless, the insurance industry is experiencing a seismic shift, driven by advancements in machine learning and AI. The once futuristic vision of a fully automated insurance company, capable of operating with minimal human intervention, is becoming a reality. Intensive research and development initiatives are paving the way for this transformation, offering the potential to revolutionize how insurance is underwritten, sold, and serviced.

AI enhances prediction accuracy through pattern recognition in historical data, facilitating more informed risk assessments. Moreover, AI automation can streamline mundane tasks such as reminders and premium payment verifications, allowing staff to focus on higher-order, creative tasks. AI analytics can quickly and efficiently process vast amounts of data, identifying patterns and correlations that would likely be missed by non-AI analytics.

The availability of big data, combined with advancements in AI analytics and the resulting predictive insights, opens new exciting opportunities. However, this evolving landscape also increases existing risks and introduces new challenges that will likely result in increased regulatory scrutiny and legislative tightening. For instance, there are concerns about the appropriateness of the data being used and analysed, including both the insurer's base data and the data it augments. Issues such as underlying assumptions or biases in predictive models, the scope of coverage provided, and the determination of coverage eligibility all raise regulatory questions (Wilkinson et al., 2024).

Additionally, significant concerns around data protection, privacy, and cybersecurity arise concerning the personal data used and generated by AI analytics. Issues of bias, fairness, discrimination, intrusiveness, and the contextual integrity of AI-generated results are also prominent (Wilkinson et al., 2024).

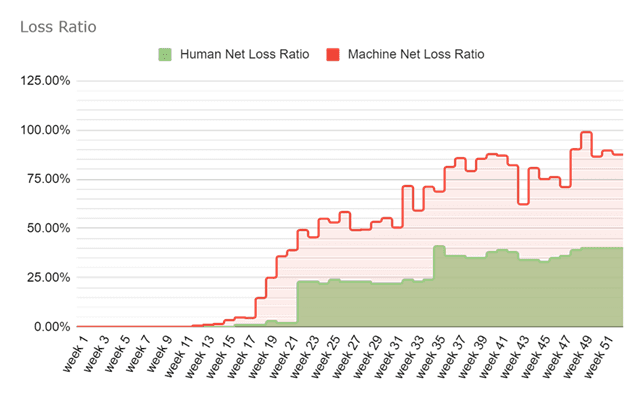

Sun Marine Automatic Algorithmic Underwriting experiment

We conducted a year-long simulation of our AI underwriter in preparation for the InsureTech Connect Asia 2023. We placed our AI system in an autonomous underwriting "as if" sandbox and fed it all incoming inquiries containing underlying data from the year 2020. The outcomes obtained by the AI underwriter over one year were compared with those achieved by human underwriters.

The AI underwriter was almost on par with humans, writing just 17% less premium. AI underwriter would have reduced attrition losses count by two-thirds within a year, compared to human underwriters. However, dramatic mid-year loss ratio spikes led to a more than double in net loss ratio compared to human underwriters.

The experiment demonstrates that effective use of AI requires training on diverse datasets that reflect the complexity and variability of real-world environments. However, collecting such data is challenging, and ensuring it is representative and unbiased is difficult for humans to validate manually.

AI boom: can it be a new market bubble?

A rally in U.S. stocks, driven by excitement for AI, is drawing comparisons to the dot-com bubble of two decades ago, raising concerns about whether prices are being overly inflated by optimism over a groundbreaking technology. While today's market doesn't entirely mirror the dot-com bubble, the enthusiasm for AI is evident and it parallels the dot-com boom of the late 1990s. Back then, the market saw a rapid increase driven by internet hype. Today, a similar trend is seen with AI, as many companies promote their AI strategies. Market corrections occur when reality doesn't meet high expectations. In 2000, lofty sales growth expectations gave way to more realistic valuations very fast and caught some stakeholders by surprise (Krauskopf, 2024; Mackintosh, 2024).

The excitement around AI, combined with a robust economy and stronger corporate earnings, has propelled the S&P 500 index to new highs in 2024, rising over 50% from its October 2022 low. Meanwhile, Nasdaq Composite index has surged more than 70% since the end of 2022 (Krauskopf, 2024).

While the future of AI remains uncertain for now, the worry is that the AI-fueled surge might end similarly to the dot-com boom, which culminated in a dramatic crash. In 2002, the Nasdaq Composite, after nearly quadrupling in just over three years, plummeted almost 80% from its March 2000. Similarly, the S&P 500, which had doubled over a similar period, fell nearly 50%. While some internet companies, like Amazon, survived and eventually thrived, many others never recovered (Krauskopf, 2024).

Earnings per share in sectors like technology, communication services, and consumer discretionary — today's market leaders — have been increasing faster since early 2023 than the broader market, according to Capital Economics. In contrast, during the late 1990s and early 2000s, earnings in these sectors grew at a similar pace to the rest of the market, although their stock valuations soared more rapidly (Krauskopf, 2024).

In May 2024, four major tech stocks added more market value than the rest of the S&P 500 combined, with Nvidia contributing more than half of this gain. Two years ago, Nvidia was valued at $400 billion; now, it is worth $3.3 trillion and is the world's most valuable company. The broader stock market's fate could be heavily influenced by any significant changes at Nvidia (Armstrong, 2024; Mackintosh, 2024).

Currently, the S&P 500's price-to-earnings ratio is 21, higher than the historical average but below the peak of around 25 seen in 1999 and 2000. The prevailing opinion is that this tech bubble will not burst until the overall market valuation reaches levels similar to those in 2000. Investor sentiment during the dot-com boom was markedly more euphoric. For instance, the American Association of Individual Investors' bullish sentiment survey hit 75% in January 2000, just before the market peaked, compared to a recent reading of 44.5%, which is above the historical average of 37.5% (Krauskopf, 2024).

Potential issues with AI include the risk of demand declining due to overhype, increased competition driving down prices, suppliers demanding a larger share of revenue, and the scalability of AI not meeting expectations (Roberts, 2024).

A limited understanding of AI's intricacies poses challenges for informed decision-making in market valuation and investment strategies. AI is seen as "popular," "progressive," and "high-potential," but this perception may cloud long-term investment judgments.

Conclusion

At first glance, it may look like we have already reached a moment in time where AI is intelligent enough to create and analyse information on par with humans. Reality is more complex than that. Indeed, AI boosts creativity and productivity, and in time, it will be able to transform every aspect of work, from making predictions to creating analytical papers and presentations. As we go from experimentation with AI models to actual business implementation, companies that embrace AI will gain a significant advantage. On the other hand, the pace of AI development that looks so promising now can stale or even hit a yet unknown hurdle.

Numerous institutions have already adopted analytical AI technologies before the current AI boom. The proliferation of AI tools continues, while they become more complex and advanced. While some believe we are on the verge of achieving artificial general intelligence (AGI) — an AI that can understand, learn, and apply knowledge across a wide range of tasks as effectively as a human — the reality is that AI is still in its early stages, and there is a long journey ahead before we fully realise its potential.

As AI takes over the more repetitive or mundane tasks, humans steer towards roles that demand creative problem-solving. Judging from the adoption of other technologies, this divergence in job roles will probably continue, with human supervision and attendance to the most complex and non-standard projects continuing to be a crucial part of AI-enhanced business.

Despite the overall promising outlook of the AI industry, the high expectations surrounding AI can lead to unrealistic forecasts for its future growth, potentially resulting in disappointment. While AI offers tremendous potential, its limitations and complexities may overshadow overly ambitious promises. Stakeholders must maintain a realistic perspective on what AI can deliver, ensuring that expectations are grounded in the technology's actual capabilities and developmental trajectory.

Analytical AI demonstrates remarkable capabilities and potential. Machine learning has applications across various fields, including insurance, and continues to evolve. In insurance, for instance, AI can improve risk assessment, streamline claims processing, and enhance customer service through predictive analytics and automation. Despite these advancements, it is important to remember that AI is a tool, not a magic solution. Patience and a balanced approach are essential; we must not place all our hopes on a single technological advancement.

References

Armstrong, R. It’s an AI market now. Financial Times (2024).

Goncalo, R. Understanding The Limitations Of Generative AI. Forbes. (2024).

Krauskopf, L. Echoes of dotcom bubble haunt AI-driven US stock market. Reuters. (2024).

Microsoft. AI at work is here. now comes the hard part. (2024)

Roberts, L. It’s Not 2000. But There Are Similarities. (2024)